Every time Liu Busi, a retail investor in the initial public offering (IPO) market in Hong Kong, checks the result of his new stock subscription, he feels a mix of uncertainty and excitement.

Joining the IPO subscription game this year amid intense oversubscription, Liu has subscribed to 25 new listings and was allocated shares in 17 of them, including CATL and Zijin Gold, the two largest IPOs in 2025, with approximately HK$ 41 billion and HK$ 25 billion raised respectively.

Of the 17 allocations, 14 have gained value after subscription, with his best performing IPO investment - Bloks, a Chinese toy company, having generated HK$ 11,059 for him as of Nov. 6.

However, Liu noticed a sharp change in his subscription success rate after Hong Kong Stock Exchange's (HKEX) new reforms on IPOs in August.

The HKEX implemented new optimisation measures on stock allocation and subscription mechanisms, including stipulating that issuers must allocate at least 40% of the shares in the IPO to the book-building placement portion and introducing two public subscription mechanism options.

Before the reform, Liu was allocated shares in 10 out of 13 subscriptions, a 77% success rate. After the reform, he could only secure allocations for 7 out of 12 subscriptions, a 58% success rate.

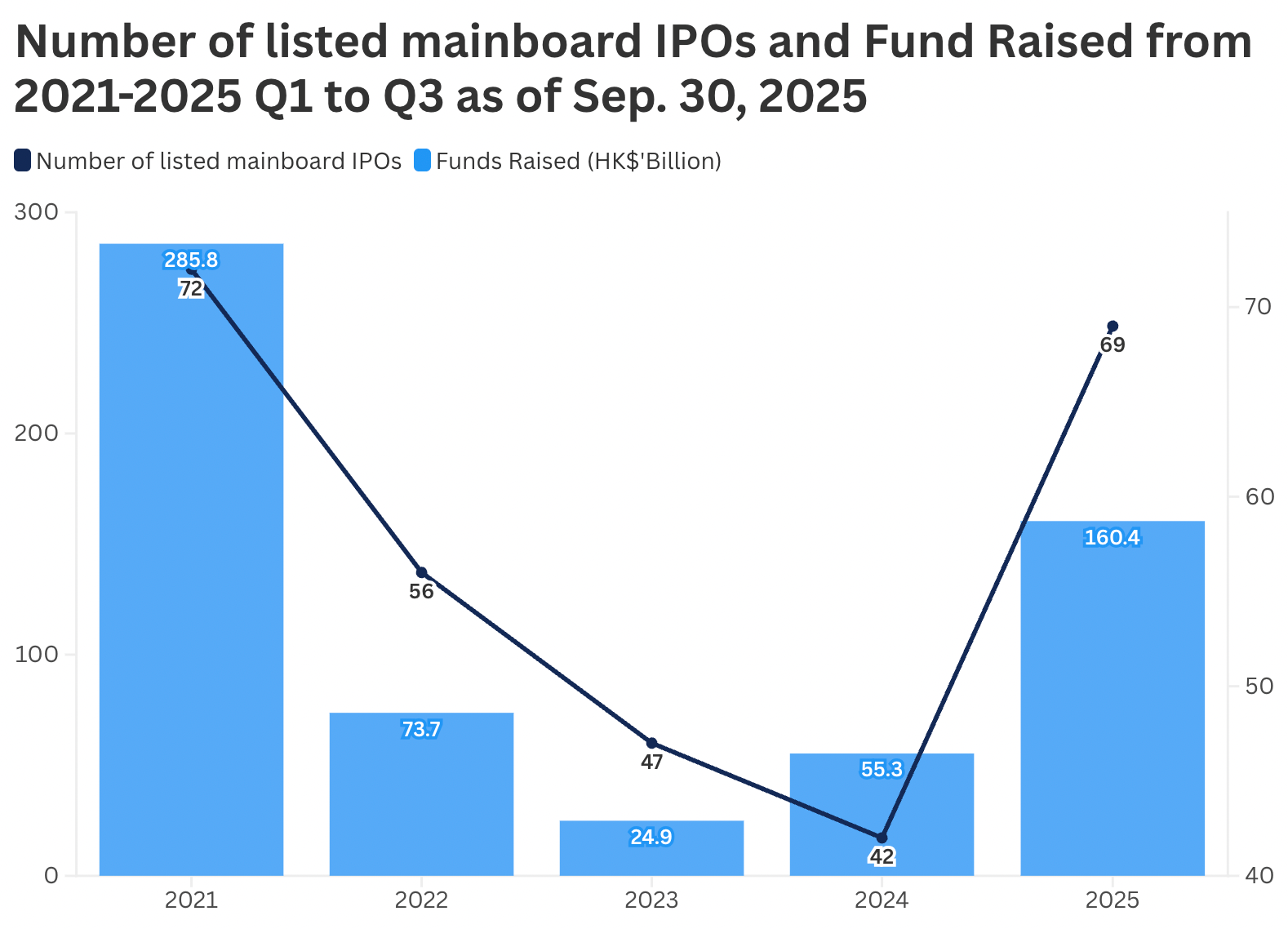

The city has seen 69 IPOs raise over HK$160.4 billion as of Sept. 30, a 183% surge compared with last year. According to Deloitte China's analysis, the city is projected to see over 80 IPOs raising HK$250 billion to HK$280 billion for the full year 2025.

HKEX did not comment on the reduced success rate of subscriptions by retail investors when asked by TYFP reporters. In an earlier news release, Katherine Ng, HKEX Head of Listing, said the exchange “has sought to enhance the robustness of the IPO pricing and allocation mechanisms, whilst supporting balanced participation from a broad range of local and international investors. At the same time, we have revised the initial public float requirements to provide issuers with greater flexibility and certainty in structuring their public offerings, and introduced a new initial free float requirement to ensure there are sufficient tradeable shares upon listing”.

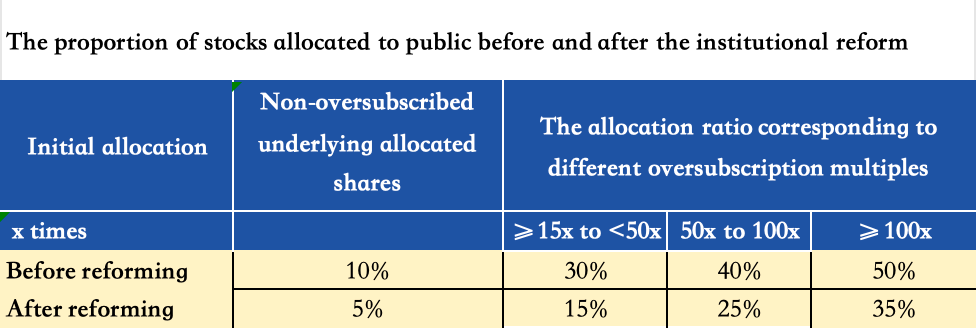

In the new regulations, Mechanism A provides for an initial allocation of 5% to the public subscription tranche with a clawback rate up to 35%, increasing the proportion of the public offering based on the oversubscription rate. While mechanism B has no clawback, it sets the initial allocation between 10% and 60%.

“This reform is related to the current booming stock market environment,” said Wayne Yu, the director at the College of Business at City University of Hong Kong.

Yu added that since there have been cases of sharp rises and falls in stock prices within a short period after going public, it has become necessary to reform IPO rules in line with market trends.

Among the 17 companies that adopted the new regulations, only SICC and AUX Electric chose mechanism A, while the remaining 15 companies all chose mechanism B.

Many of these Mechanism B companies selected the lowest allowable public allocation of 10%. Examples include Guangzhou Innogen Pharmaceutical Group Co., Ltd., Shuangdeng Group Co. Ltd., Jiaxin International Resources Investment Ltd. , and Chery Automobile Co Ltd., all of which set their public offerings at this minimum level, resulting in allocation rates of 0.06% to 1%.

Kenny Wen, an executive committee member of the Hong Kong Society of Financial Analysts, believed that this reform is unfair to retail investors.

“Regulators believe that giving too much stock to retail investors could lead to excessive stock price increases, so they want to allocate a larger portion to institutional investors, hoping to keep the price stable,” said Wen.

That means, Wen added, retail investors who didn't win the lot but want to buy shares will have to buy them in the secondary market at a higher price after listing.

Duan Yang, associate director of the department of finance at Hong Kong Baptist University, also agreed that the primary purpose of the reform is not to harm retail investors' interests but to reduce price volatility and enhance stock market efficiency.

“We will face increasingly lower lot winning rates and uncertain returns as policies further tilt towards institutions,” said Wendy Guo, a retail IPO investor. She believes retail investors have limited influence in the market because they represent only a small portion of total investment capital.

Before the new regulation took effect, 53 IPOs in 2025 had an average one-lot success rate of 30.69% for retail investors. After the regulation, the 17 IPOs completed as of Oct. 10 under the new mechanism saw this rate drop to 7.89%, according to TYFP's analysis.

Only three of these 17 companies—Zijin Gold International, Hesai-W, and AUX Electric—maintained success rates above 30%, while the remaining 14 companies had rates between 0.02% and 1%.

Despite the decline in the subscription success rate, both Liu and Guo continue to invest in the Hong Kong IPO market.

“The new rules merely alter the distribution ratio of the ‘pie’,” Liu said. “Although retail investors receive a smaller share, they still get a portion, and it remains a low-risk investment.”

Guo has adjusted her investment strategy, allocating part of her funds to the secondary market and buying some blue-chip stocks with relatively stable performance, while still participating in new share subscriptions.

Since 2025, the average net profit per lot for retail investors who won IPOs under the old mechanism was HK$1050.45. Under the new regulations, as of Oct. 10, this figure reached HK$4216.64, an increase of 249.1% compared to the previous period.

Yu, from City University of Hong Kong, noted that although the share of retail investors has decreased compared to before, it is still significantly higher than in major developed countries such as the US and Canada.

Wen also advised retail investors against blindly chasing stocks that have surged after high-priced IPO listings, suggesting they preserve their capital for future opportunities.

Wen also called for the regulators to ensure investors are treated equally.

“Regulators think more stocks should be given to rational institutional investors, but judging retail investors as irrational is an irrational judgment itself,” he said.

《The Young Reporter》

The Young Reporter (TYR) started as a newspaper in 1969. Today, it is published across multiple media platforms and updated constantly to bring the latest news and analyses to its readers.

From concert dreams to criminal threats: Hong Kong students trapped in cross-border scams

Chinese Gen Z shifts focus to lesser-known European destinations amid social media trend

Comments