Zhou Haoming, a marketing and editing position in a publishing company at Park Commercial Centre in Tin Hau, observed that an increasing number of companies had moved out of the building over the past six months, leaving the premises noticeably quieter and less populated.

After the companies moved away, the number of partner businesses in the office building, with which Zhou’s company could jointly carry out promotional activities, decreased significantly.

Corporate relocation activity was active in 2025. AIA Hong Kong announced in 2024 that it would expand into AIRSIDE, an A-grade commercial building in Kai Tak, as a new operations and training base for its financial planners. Activities gradually moved into the new office in 2025. Cory Tsai, a financial planner at AIA, said the new location offers better transport connectivity and amenities, as Kai Tak is now regarded as Hong Kong’s new economic centre.

AIA’s relocation to new business areas is not an isolated case. Since the second half of 2025, Hong Kong’s office market has seen a period of heightened activity driven by large-scale leasing transactions and relocations.

Among the more notable cases is UBS, which announced on February 3, 2026, that it would relocate and consolidate all of its Hong Kong offices into a single hub at the International Gateway Centre in West Kowloon.

Sam Gourlay, JLL Head of Office Leasing Advisory, also noted that more firms are expanding to emerging business centers such as West Kowloon and Tsim Sha Tsui, drawn by their strategic connectivity and access to the high-speed rail link to mainland China.

While Hong Kong’s office market has found some stability supported by such high-profile leasing deals, the improvement has come mostly from corporate relocations, Gourlay said.

JLL said in its press release that the office market showed a gradual recovery in the third quarter of 2025, with total net absorption rising 137.5% quarter-on-quarter to 646,000 square feet, rebounding from the weak first half.

Grade A offices recorded about 1.8 million square feet of positive net absorption in 2025, the highest level since the pandemic.

Net absorption reflects the change in leased office space, calculated as newly leased area minus vacated space. Stronger absorption indicates rising demand.

Ernest Tse, senior divisional sales director of the office department at Centaline Commercial, said financial institutions, securities firms, and companies involved in initial public offering (IPO)-related activities remain the primary sources of office demand. By contrast, traditional industries such as trading face tighter economic constraints and thus greater difficulty affording office rents.

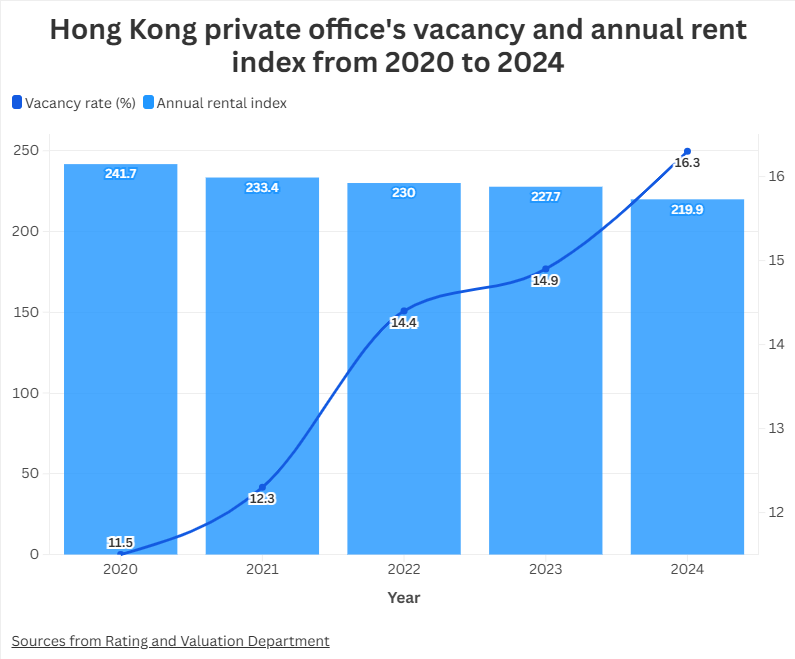

However, due to a substantial influx of new supply, the market has witnessed a significant supply glut, pushing the vacancy rate from roughly 10% pre-pandemic to 17.3%, indicating that the recovery remains limited.

Beyond relocations to emerging areas, another prominent trend driving leasing activity is the return to traditional core districts.

According to Tse, Hong Kong’s traditional office core districts comprise Central, Admiralty, Sheung Wan, and Causeway Bay on Hong Kong Island, plus Tsim Sha Tsui and East Tsim Sha Tsui in Kowloon, with all other areas classified as non-core.

Tse noted that amid a muted economic climate, rents in core districts such as Central have declined notably, prompting companies to rethink their location strategies.

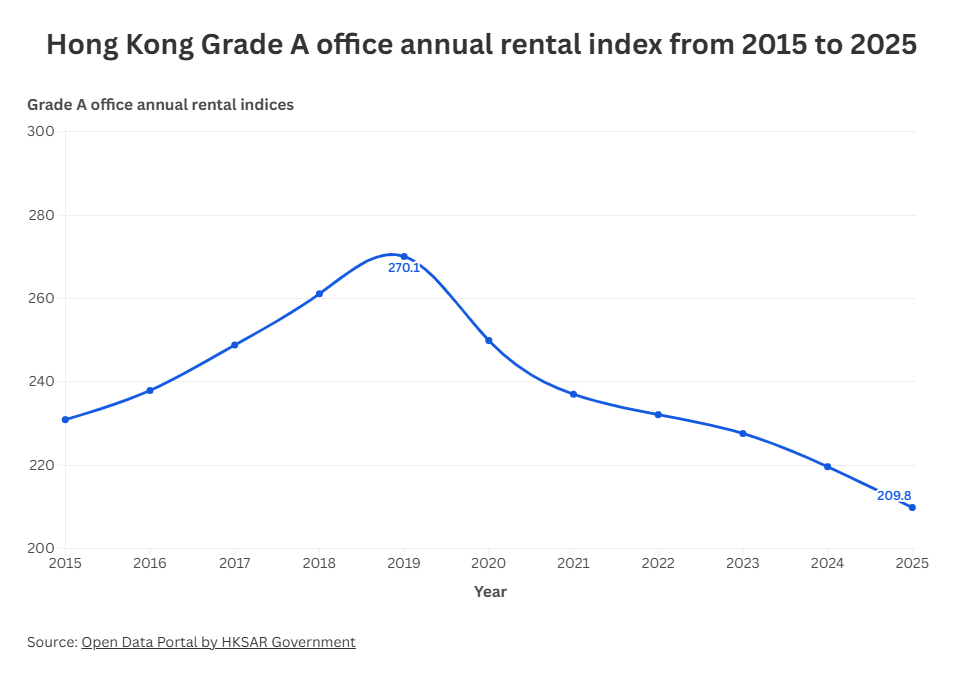

The government data show that the Grade A office rents in Central have declined notably from HK$1,201 per square metre in 2020 to HK$858 per square metre in 2025.

Consequently, many firms are consolidating their scattered offices in Wan Chai and Causeway Bay and relocating back to Central or Admiralty.

JLL showed in its press release that Central recorded 0.5% rental growth in the second half of 2025, with its vacancy rate falling to 10.9%. Conversely, decentralised areas like Hong Kong East and Kowloon East continue to experience significant rental corrections and high vacancy rates.

“Although rents in core districts may still be higher than in many non-core areas, the decline from past peaks has been substantial,” Tse added.

Tse also pointed out a trend of many companies downsizing their office space during relocation, trading a reduction in leased area for better premises.

“Previously, they might have had 12,000 square feet across Wan Chai and Causeway Bay. Now 7,000 to 8,000 square feet is sufficient, while still maintaining a strong corporate image and a prime location,” he said.

Yet, Tse noted that space vacated in non-core districts often struggles to find new tenants quickly. As a result, the overall market may appear active due to surging relocation-related leasing activity, but vacancy remains elevated, especially in non-core districts.

The latest data from Centaline Commercial showed that in December 2025, the Grade A office vacancy rate was around 12% in Central and approximately 23% in Kowloon Bay.

Addressing the vacancy issue in non-core districts, Tsang Tak-ming, an associate professor at the Chinese University of Hong Kong’s Centre for Hospitality and Real Estate Research, suggested that tackling non-core vacancies requires transformation and industrial diversification.

“Focusing on some new industries would be one way to diversify the pie (to better utilise the vacant office space),” he said.

He mentioned that as the education sector expands, many Hong Kong universities are acquiring and repurposing office buildings for teaching and student accommodation, marking a key direction for transformation in the office market.

Looking ahead, Tsang said Hong Kong’s office market remains resilient.

“Hong Kong (Hong Kong’s office market) still has promise,” Tsang added. “ After all, it is still a big financial hub, and there are still many people doing business here.”

Tsang believed that if these new firms keep growing and both the government and industries diversify beyond finance into sectors like education, technology, and eventually creative industries, it could support the office market.

Gourlay, however, remains cautious about the sustainability of the recovery.

He said that the biggest risk lies in demand being overly concentrated in a small number of large transactions.

“Everyone is getting very excited about one or two major transactions, but they have been in this algorithm, and trading, quant funds phase,” he added. “We have a really small subset driving the overall demand, and the big risk is that it doesn’t broaden beyond that.”

《The Young Reporter》

The Young Reporter (TYR) started as a newspaper in 1969. Today, it is published across multiple media platforms and updated constantly to bring the latest news and analyses to its readers.

Singapore’s dining shake-up: How a wave of foreign brands is reshaping the food scene

Would you like to be “friends with badminton”? Hong Kong focuses on abstinence, not sex education

Comments